Is the spring housing market ready for the Fed’s déjà vu?

It’s spring 2024 and we have a Federal Reserve meeting this week. The 10-year yield is at the same critical point as last year before the Fed went hawkish and sent mortgage rates to 8% and the 10-year yield to 5%. Could this happen again? This is the week the balls are all in the Federal Reserve’s court. I believe it is in the Fed’s interest to keep existing home sales depressed. Here is the interview I gave on CNBC on the day the Fed went hawkish, explaining why.

A serious 10-year yield and mortgage rate talk

My work on housing moves around the 10-year yield and the economics that move that. The growth rate of inflation has fallen a lot on the year-over-year data, but mortgage rates haven’t gone down, which isn’t surprising to me as my mantra has been: “Labor over Inflation.”

For 2024, the 10-year yield running between 3.80%-4.25% looks perfectly normal to me as long as the economic data is firm and the Fed hasn’t pivoted. I can’t see the 10-year yield below 3.37% unless the labor market breaks — meaning jobless claims over 323,000 on the four-week moving average. That means I can’t see mortgage rates going below 6%, especially with the spreads being bad, until the labor market or the economy gets weaker.

However, now we are at the same spot as last year, near the critical 4.34% level and we have the Federal Reserve meeting coming up. This is a big week, as you can see in the chart below.

With mortgage rates above 7% again, we will have to see what the Fed says at this meeting because, in the past few meetings, they have made it clear that policy is restrained and that they don’t want it to get too restrictive. This is what happened last year when the 10-year yield headed to 5% and we had 8% mortgage rates. However, there is a risk of the Fed sounding too hawkish again which would send the 10-year yield higher.

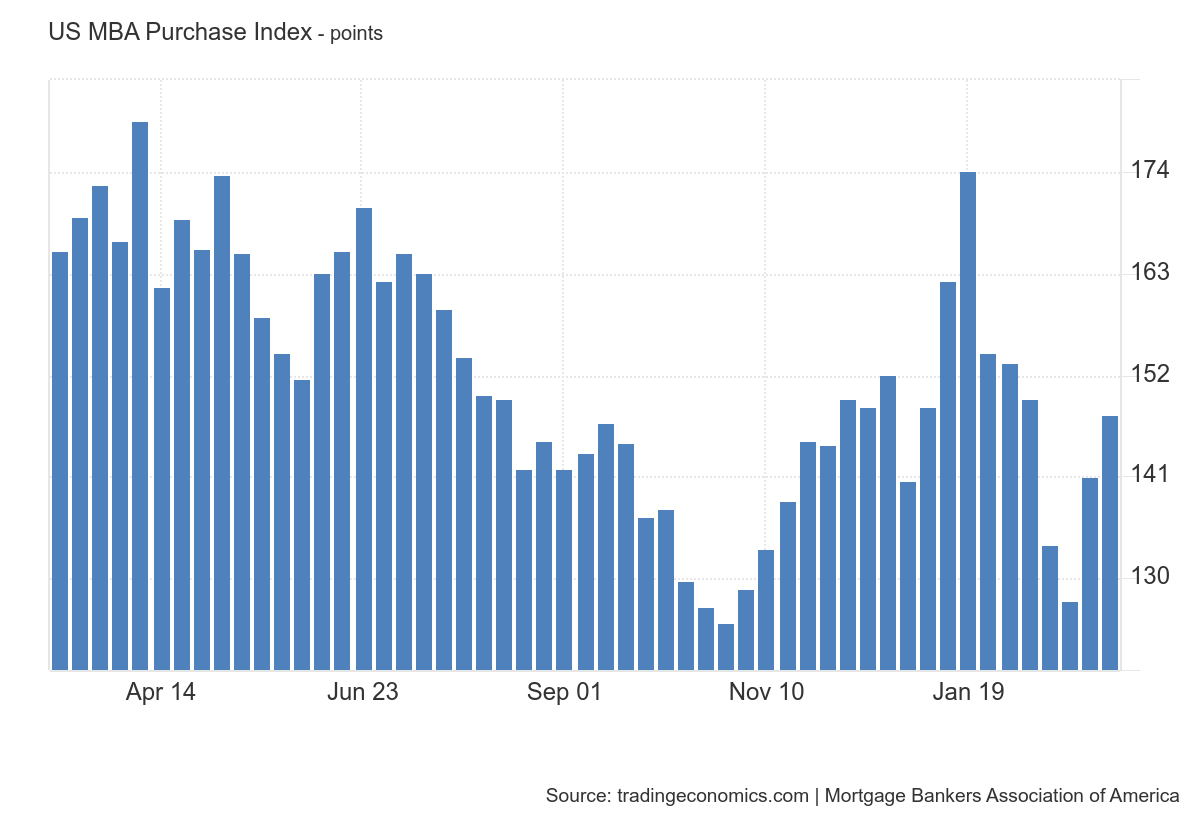

Purchase application data

As mortgage rates have been falling recently, we saw back-to-back weeks of growth in the purchase application data, which aligns with what we saw last year. Remember, we are working from extremely depressed levels in this data line, so the bar is so low that it doesn’t take much to move the needle.

Since November 2023, we have had 10 positive and five negative purchase application prints after making holiday adjustments. Year to date, we have had four positive prints versus five negative prints. Clearly, if mortgage rates can head toward 6% and hold we will get rising demand, but I believe the Federal Reserve wouldn’t be able to sleep at night if more people were buying homes.

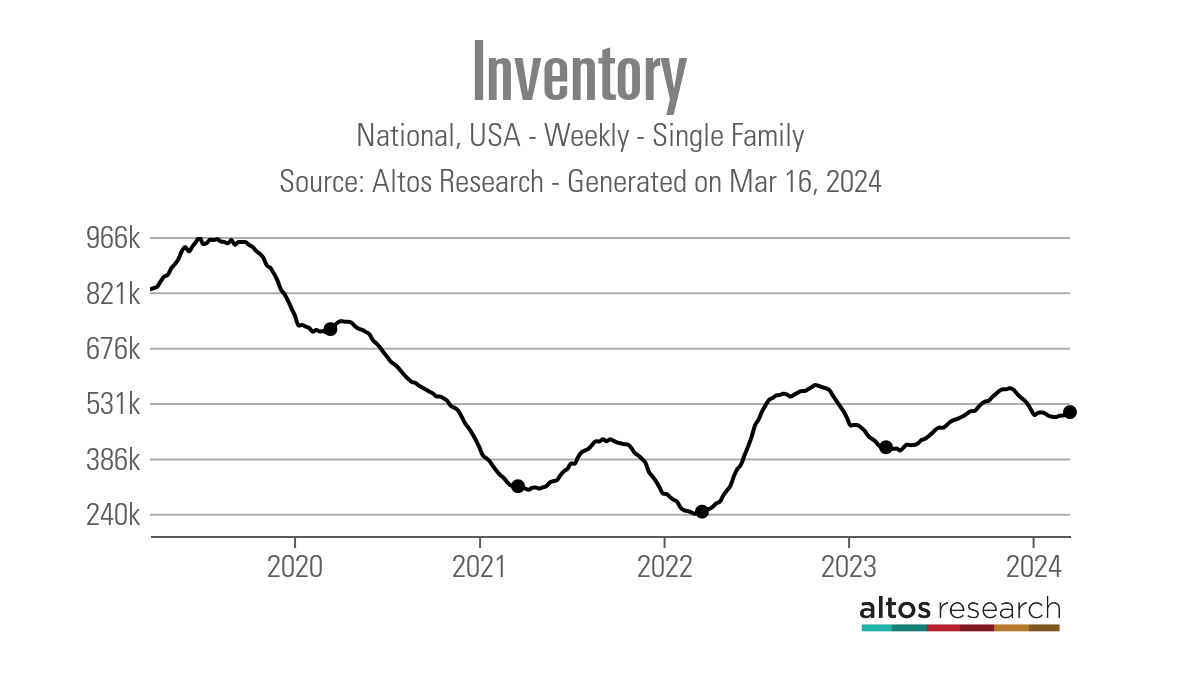

Weekly housing inventory data

The one positive story for me in housing this year is that inventory is growing year over year for both active inventory and new listing data. I know it’s not a lot, but growth is growth. The one benefit of higher rates is that inventory can grow in the post-2010 qualified mortgage world as long as higher rates create softness in demand. It hasn’t been a lot of growth historically, but growth is growth.

Last year, the seasonal inventory bottom happened on April 14, which was the the longest time to find a seasonal bottom ever. This means we will show more than normal inventory growth until we get past tax day 2024.

Here is a look at the inventory last week:

- Weekly inventory change (March 8-15 ): Inventory rose from 500,579 to 507,160

- The same week last year (March 9-16): Inventory rose from 413,199 to 414,967

- The all-time inventory bottom was in 2022 at 240,194

- The inventory peak for 2023 was 569,898

- For some context, active listings for this week in 2015 were 982,639

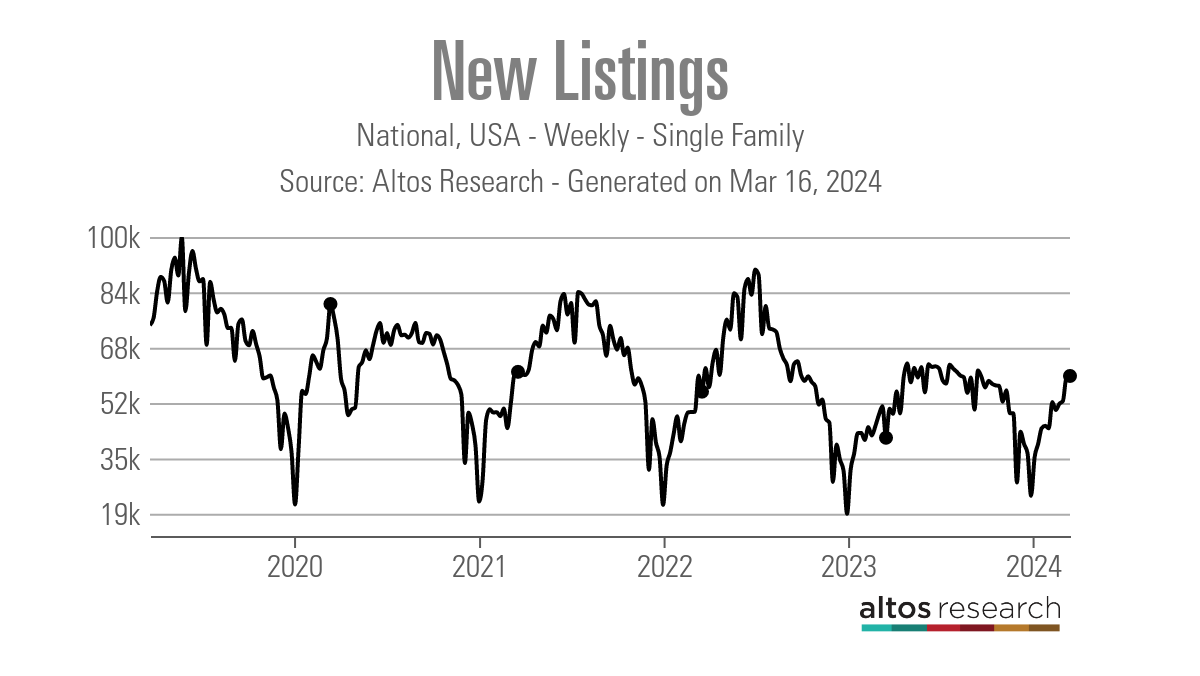

New listings data

New listings are growing yearly, which is another plus for housing. Last year, II picked up on the trend that new listing data was creating a historical bottom as the data line wasn’t heading lower with higher rates. The growth is a tad lighter than what I was hoping for. But as someone who didn’t buy the mortgage rate lockdown premise that inventory can’t grow with higher rates, this year is a good test case.

Here’s the weekly new listing data for last week over several previous years:

- 2024: 59,542

- 2023: 41,415

- 2022: 54,542

For some historical context, new listing data this week in 2010 was 306,020.

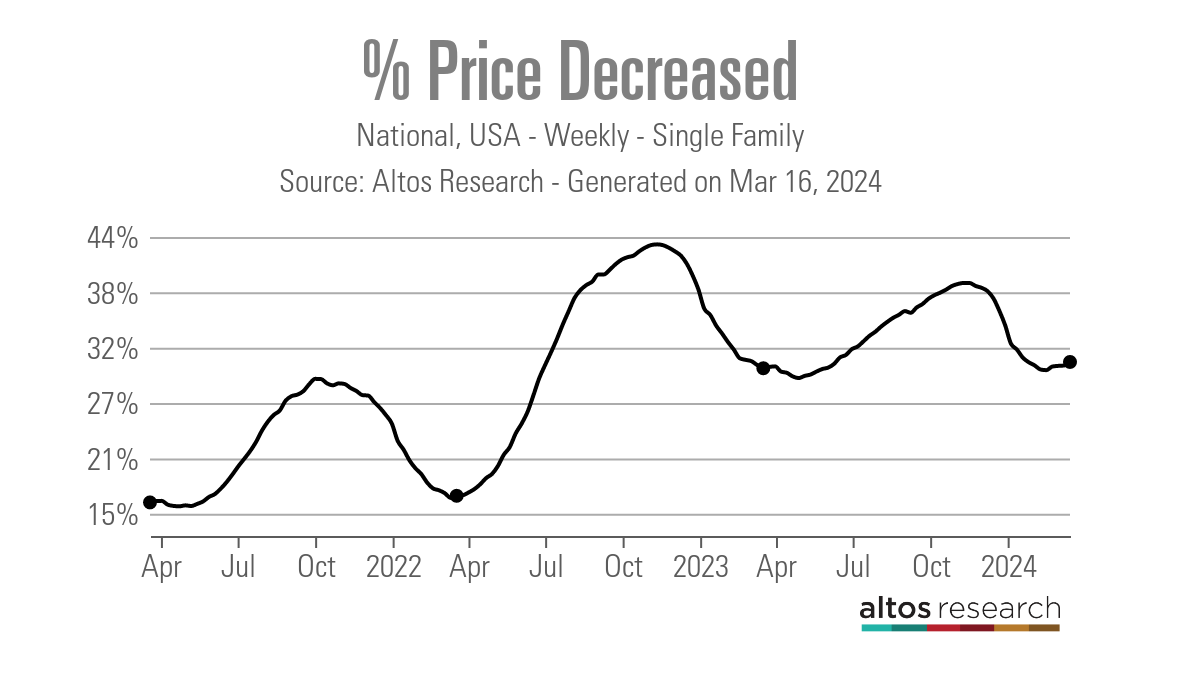

Price-cut percentage

Every year, one-third of all homes take a price cut before selling — this is regular housing activity and this data line is very seasonal. The price-cut percentage can grow when mortgage rates move higher and demand gets hit. When rates fall, they go lower than an average year.

Inventory is higher than last year, and we might have found the bottom already, so as the year progresses, the number of homes taking a price cut should increase. The goal is to see how the mortgage rate variable plays into this data line. This is why this week’s Fed meeting is key, to see if the 10-year yield can break higher, which should increase the price-cut data.

Here’s the percentage of homes that took a price cut before selling last week and how that compares to the same week in previous years:

- 2024: 31%

- 2023: 30%

- 2022: 17%

Week ahead: The Fed and housing data

The Federal Reserve’s language and the dot plot are the two things to watch this week. The dot plot should still show many Fed members having two to three rate cuts in play for 2024, with some going the opposite way from that group. We also will have tons of housing data coming out this week, including the builders’ confidence, housing starts, existing home sales, and Zillow home price data. However, the key is the Fed, Fed and the Fed!