Housing Market Tracker: Banking crisis is a new variable

The housing market was crazy again last week. Mortgage rates fell as the banking crisis got worse and purchase application data grew for the second week in a row, but the big question is: Did we hit the seasonal bottom in housing inventory?

Here’s a quick rundown of the last week:

- The 10-year yield had a roller-coaster week, and so did mortgage rates, but the 10-year yield held its critical line, and mortgage rates ended at 6.55%.

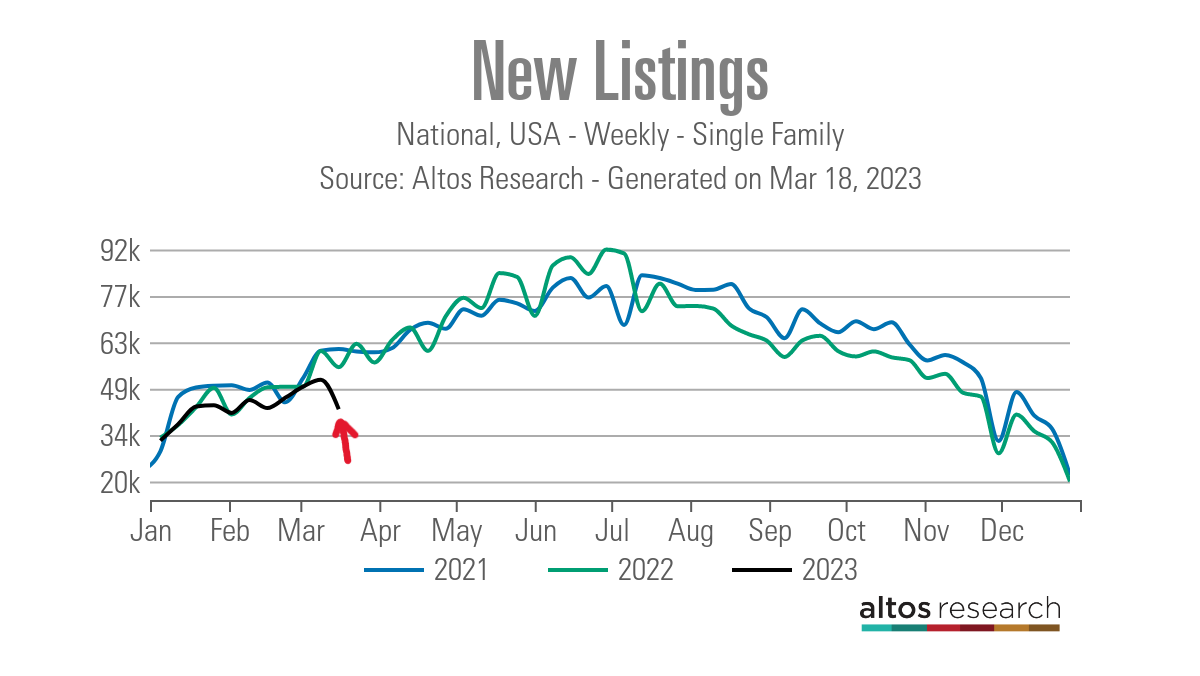

- Weekly inventory increased by 1,734. New listing data collapsed, but we are putting an asterisk on that data line for this week.

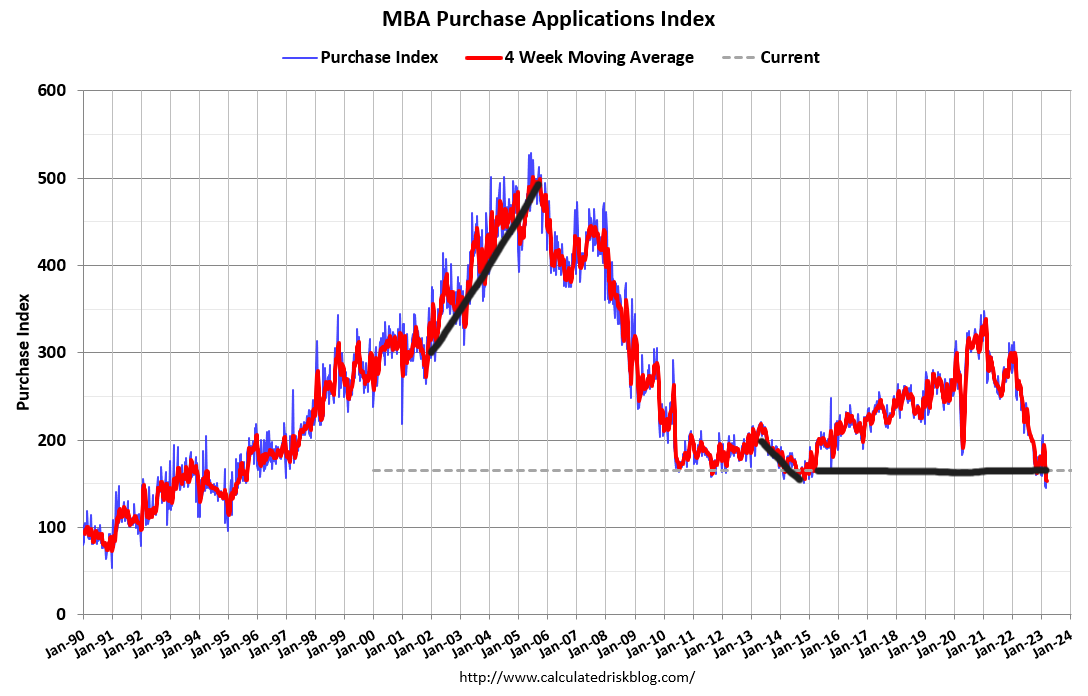

- Purchase application data rose 7% weekly, still down 38% year over year.

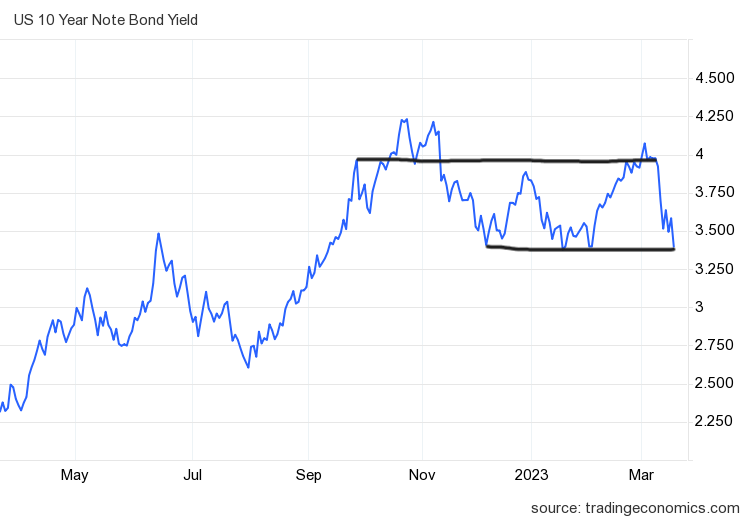

10-year yield and mortgage rates

A national banking crisis while the Federal Reserve raises rates and reduces its balance sheet sounds like a lousy cocktail for economics, but that is precisely what we are dealing with today. As I write this article, I see news that even Warren Buffet has been asked to chime in on how to deal with this crisis.

So, we can now add a new variable into the equation for 2023: What does a banking crisis mean for mortgage rates?

In my 2023 forecast, I said that if the economy stays firm, the 10-year yield range should be between 3.21% and 4.25%, equating to mortgage rates of 5.75% to 7.25%. If the economy gets weaker and we see a rise in jobless claims, the 10-year yield should go as low as 2.73%, translating to 5.25% mortgage rates. This assumes the spreads are wide as the mortgage-back securities market is still very stressed.

The economic data was OK last week. If we didn’t have the banking crisis, we would probably just focus on how firm the economic data was last week. GDP growth was estimated at 3.2%, jobless claims fell last week, housing starts beat estimates and purchase application data showed some growth. Retail sales were slightly below estimates, but we had positive revisions, and industrial production was unchanged.

Last week’s 10-year yield took us to the critical line in the sand.

Last week the two-year yield collapsed from a 5% level to under 4%. This bond market is screaming at the Fed to cut rates. However, many Wall Street firms were betting on higher rates and got burned by the banking crisis. So, the market is wild and the Fed might not care what short-term rates are doing now.

Mortgage rates fell and ended the week at 6.55%, however, we see a lot of stress in the financial markets. Many people wondered why mortgage rates weren’t lower on Friday; the answer is that the banking crisis has stressed the mortgage-backed securities market more than when bond yields fell to these levels last time.

So this is going to be an epic week because we have incorporated a new variable into 2023 that wasn’t in the equation at the start of the year and the Fed meets on Tuesday and Wednesday.

I want to see how the 10-year yield acts this week. Can we get follow-through bond buying, which would take a direct shot at the low-level range of 3.21%? That would be a big deal to me because it’s happening with the labor market still doing OK.

We don’t know what news can happen at any second to change the landscape of the economic discussion until the financial markets calm down.

With the potential of news getting worse in the short term, we need to be mindful that we can see some crazy market pricing in mortgage rates and moves in the 10-year yield. So, every day counts now during a banking crisis, as the world markets are trying to restore some order.

Weekly housing inventory

Looking at the Altos Research data from last week, the big question is whether we are finally starting to see the seasonal increase in spring inventory. On this front we have some good news and some bad news.

First, we saw a slightly increased number of active listings, which made me jump for joy! Last March is when we saw the seasonal bottom before inventory took off, so I am hoping we get the same growth in the data this week, making it back-to-back years that we bottomed out in March. Although that’s not normal, it’s better than what we saw in 2021 when we didn’t hit bottom until April.

- Weekly inventory change (March 10-March 17): Rose from 412,535 to 414,278

- Same week last year (March 11-18th): Fell from 247,320 to 245,776

- The bottom for 2022 was 240,194

The seasonal increase in inventory means more sellers can also be buyers of homes and fewer bidding wars in certain parts of the country.

Now the bad news: new listing data fell so much this week that I am putting an asterisk on this week’s data until we see if this is a trend or just a one-off in the weekly data that can occur from time to time.

Also, we are creating a bigger gap in the year-over-year data. Earlier in the year, we were on par or even slightly higher some weeks than the previous two years. Now we are creating a bigger gap, as you can see below:

- 2021 60,904

- 2022 55,348

- 2023 42,407

For some historical reference, these were the weekly inventory data in previous years:

- 2015 80,909

- 2016 84,647

- 2017 78,237

Now, this new listing number can be one week of data that just reverts to the trend, which would be higher than this level. Or, like last year at the end of June, when rates spiked higher, we saw a noticeable decline in new listings, since households didn’t want to list their homes with rates rising.

This is something that I have talked about before — some homeowners just don’t want to buy homes with mortgage rates of 7% plus and decide to call it to quits. This is a problem when mortgage rates move higher too quickly, and it gets harder to make that big life-long decision when the cost of housing matters.

Let’s wait two more weeks and see if this new listing trend continues or just reverts higher. I am hoping it’s just a one-week event.

Purchase application data

Last week we got better news with another 7% week-to-week gain on purchase apps, and the year-over-year decline also fell. However, as I always stress, the bar is low here, so it doesn’t take much to move the needle on application data when mortgage rates move lower.

When rates spiked from 5.99% to 7.10%, that gave us one month’s negative data week to week, but the last two weeks have been positive. We have had more positive purchase application data than negative since Nov. 9. Since this data looks out 30-90 days, this week’s existing home sales report should see a bounce.

We need to be mindful of the data coming out later in the year with the one-month decline in this index. However, you don’t need to be a rocket scientist or have a Ph.D. in economics here to realize the housing market is moving with where the 10-year yield is going, even with mortgage spreads wide. So with all the drama we have today, let’s see if mortgage rates fall further this week or whether the line in the sand holds.

The week ahead

This week we have existing home sales and new home sales reports coming out, but to be dead honest, economic data doesn’t matter until we get control of this banking crisis situation. While writing this article, news broke that UBS is buying Credit Suisse with government support and Flagstar will buy Signature Bank assets. In addition, the Fed announced a

coordinated central bank action to enhance the provision of U.S. dollar liquidity.

In times like this, market drama needs to calm down first before we can focus on the economic data. The Federal Reserve will meet this week on Tuesday and Wednesday, and the Q&A portion of this meeting will be epic.

Remember that back in November Fed Chair Powell said, “I don’t have any sense we have overtightened or moved too fast.” Now, after all the emergency banking lending programs and global coordination to keep the banking system working, does he still believe this statement? I am hoping someone asks him this direct question.

Listening to what the Fed says this week is critical. We can focus directly on the housing data, but the noise this week will determine whether the market believes this banking crisis is under control or it’s burning out of control, forcing the Fed and the government here and around the world to do more to calm the markets down.